Happy Back to School to our clients with school-aged children!

Why are we already bugging you about January 1, 2026?!

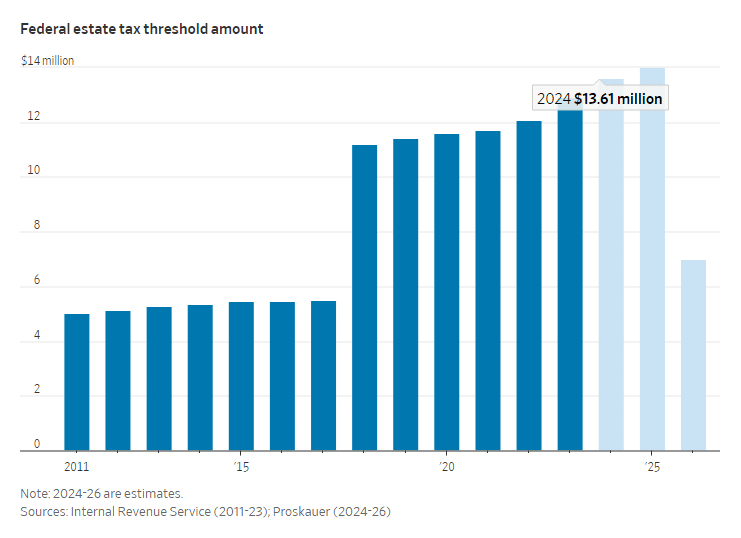

As part of the 2017 tax cut deal, the estate tax exemption (amount that an individual can give away during their life and at their death without taxes) was doubled to $10M per person and indexed with inflation through the end of 2025. The current exemption is $12.92M, but that number should be $7M at the end of 2025. As this Wall Street Journal article from last month mentions, *subscription link required (may not be required): email Lorie if you want a link to the article and don’t have a subscription to the WSJ* affluent Americans have already started to respond to this “cliff” in a big way. Statistics aren’t yet available for 2022 and 2023, but affluent Americans gifted more in 2021 (mostly through trusts) than in any year since 2013.

Is it possible the law could be changed before then? It’s possible, but you’d really be rolling the dice! I have my educated guesses, but I’m not going to place any bets on what Congress will do…there are just too many variables! I agree with what an attorney quoted in the article said: “You have to assume the exemption is going down (to $7M). If you’re banking on the exemption staying at $14 million in 2026, that is a gamble, and you’re potentially leaving a lot of tax savings on the table.”

Who should be talking with us about the coming changes in the law and whether their plan should be adjusted as a result? Individuals with a current net worth – or expected net worth in the next decade or so – (including proceeds from life insurance policies) over $6M and married couples with a current or expected net worth over $12M. Estate tax planning is unlikely to be justified for clients under those asset levels.

This chart from the article provides a clean snapshot of the estate tax landscape. You can see that the exemption was $5M (adjusted for inflation) from 2011 to 2017 before bumping up to $10M (adjusted for inflation from 2018-2025). Based on inflation estimates, the exemption would peak at $14M in 2025 before dropping to around $7M in 2026. As a result, we are talking with our high net worth clients about whether they are comfortable using a strategy to capture the currently high exemption ($12.92M) before it goes away in a couple of years. It’s a bit of a “use it or lose it” situation – and the IRS has confirmed that taxpayers who do planning based on the higher exemption will not be subject to “clawbacks” of the planning once the law changes.

What have our clients been doing to prepare for this law change?

- Annual gifting to loved ones – up to $17K per year per gift giver to each gift recipient (expect that figure to go up to $18k/year next year)

- Spousal Lifetime Access Trusts (“SLAT”) – spouses use up their high (currently $12.92M) exemption by creating a trust for the benefit of their spouse. This can be a little less scary for some clients than giving the assets to a trust for their children!

- Gifts or low-interest loans to children or other loved ones.

- Enjoying life more by spending more on themselves, giving gifts to loved ones and charities now rather than at their passing. I often share this quote with our affluent clients who are a bit on the frugal side: “If you don’t fly first class, your kids will!”

If you think the coming law changes may affect you, please reach out to us so we can start the discussions. In Person | By Zoom | By Phone

Committing to estate tax planning involves a lot of thought, consideration of pros and cons, and coordination with your other advisors. Waiting to start this conversation in 2025 isn’t likely to result in a plan that is ideal for you or your beneficiaries.

The Moves Wealthy Families Are Making to Skirt Estate Taxes

And remember, another Legacy Program benefit (and a cost of non-renewing) is that typically discussions and implementation of even somewhat minor changes to the estate plan for non-legacy program clients cost $5,000+.